Modelo 111: Spanish IRPF withholding, deadlines and 2026 boxes

Modelo 111 reports the IRPF (Spanish income-tax) withholdings you apply to payroll, professional invoices and prizes. 2026 deadlines, boxes 01-30 and current rates.

TL;DR: Modelo 111 is the Spanish self-assessment form for the IRPF (personal income tax) withholdings you apply when you pay payroll, invoices from professionals, prizes, forestry proceeds or image rights. Any organisation that withholds files it, not just the self-employed. It is quarterly as a rule (up to the 20th of April, July, October and January; the 15th if you pay by direct debit) and monthly for large companies. Boxes 01-30 group each type of income, and the annual sum of box 28 must reconcile with the Modelo 190 summary.

Key takeaways

- Any organisation that withholds IRPF on payroll, payments to professionals or prizes files Modelo 111: it is not exclusive to the self-employed (art. 76 of the IRPF Regulation).

- Quarterly filing as a rule; mandatory monthly for large companies (turnover above EUR 6,010,121.04) and public administrations with a budget above EUR 6M.

- 2026 deadlines: up to 20 April, July, October and January; up to the 15th with bank direct debit.

- Boxes 01-30: employment income (01-06), business/professional income (07-12), prizes (13-18), forestry proceeds from public woodlands (19-24), image rights (25-27); box 28 is the total and box 30 the amount payable.

- The annual sum of box 28 across the four Modelo 111 filings must reconcile with Modelo 190 (filed 1 Jan-2 Feb 2026).

- 2026 rates: employment income on a progressive scale; professionals 15% (7% for the start-up year + 2 more); agricultural/livestock 2% (1% for fattening); forestry activity 2%; flat-rate (modulos) 1%; forestry proceeds from public woodlands (boxes 19-24) 19%; prizes 19%.

Contents

Every time you run payroll, receive an invoice from a professional who has applied an income-tax withholding, or pay out a prize, that withheld money is not yours: it is an advance on the income tax of the person being paid, and you are the one who has to hand it over to the Spanish Tax Agency (AEAT, informally “Hacienda”). Modelo 111 is the self-assessment form you use to do it.

This is not a form only for freelancers. Any organisation that withholds files it, whatever its size. This guide explains who is obliged, the exact 2026 deadlines, what goes in each of boxes 01-30, and how everything reconciles with the annual summary, Modelo 190.

A note for international readers. “IRPF” (Impuesto sobre la Renta de las Personas Físicas) is Spain’s personal income tax. A “Modelo” is a numbered official tax form. When a Spanish organisation pays certain types of income, it must retain part of it at source and pay that amount to the tax authority on the recipient’s behalf. Modelo 111 is how those withholdings are declared and paid.

What Modelo 111 is and who has to file it

Modelo 111 is the periodic self-assessment of IRPF withholdings and payments on account applied to income you pay to third parties. You gather what you withheld during the period and pay it to the Tax Agency.

Under Article 76 of the IRPF Regulation (Royal Decree 439/2007), the obligation to file falls on every individual, company and entity required to withhold or make payments on account that pays out any of the following:

- Employment income (payroll, salaries, severance).

- Business and professional income (invoices from professionals that carry a withholding).

- Prizes from participation in games, contests, raffles or random draws.

- Forestry proceeds from public woodlands.

- Fees for the assignment of image-exploitation rights.

The legal basis is Order EHA/586/2011 of 9 March (BOE-A-2011-4948), which approved the form, together with the IRPF Regulation (RD 439/2007). It does not depend on any new 2026 legislation: the form and its obligations come from those texts.

Frequency: quarterly as a rule, monthly for large companies

Modelo 111 has two filing rhythms depending on the size of the withholding agent.

Quarterly as a general rule. This covers the vast majority of withholding agents.

Monthly, on a mandatory basis, for:

- Large companies: those whose turnover in the previous calendar year exceeded EUR 6,010,121.04.

- Public administrations with an annual budget above EUR 6 million.

It is the previous year’s turnover that sets the rhythm: below the threshold you file each quarter; once you exceed it, you move to declaring and paying every month.

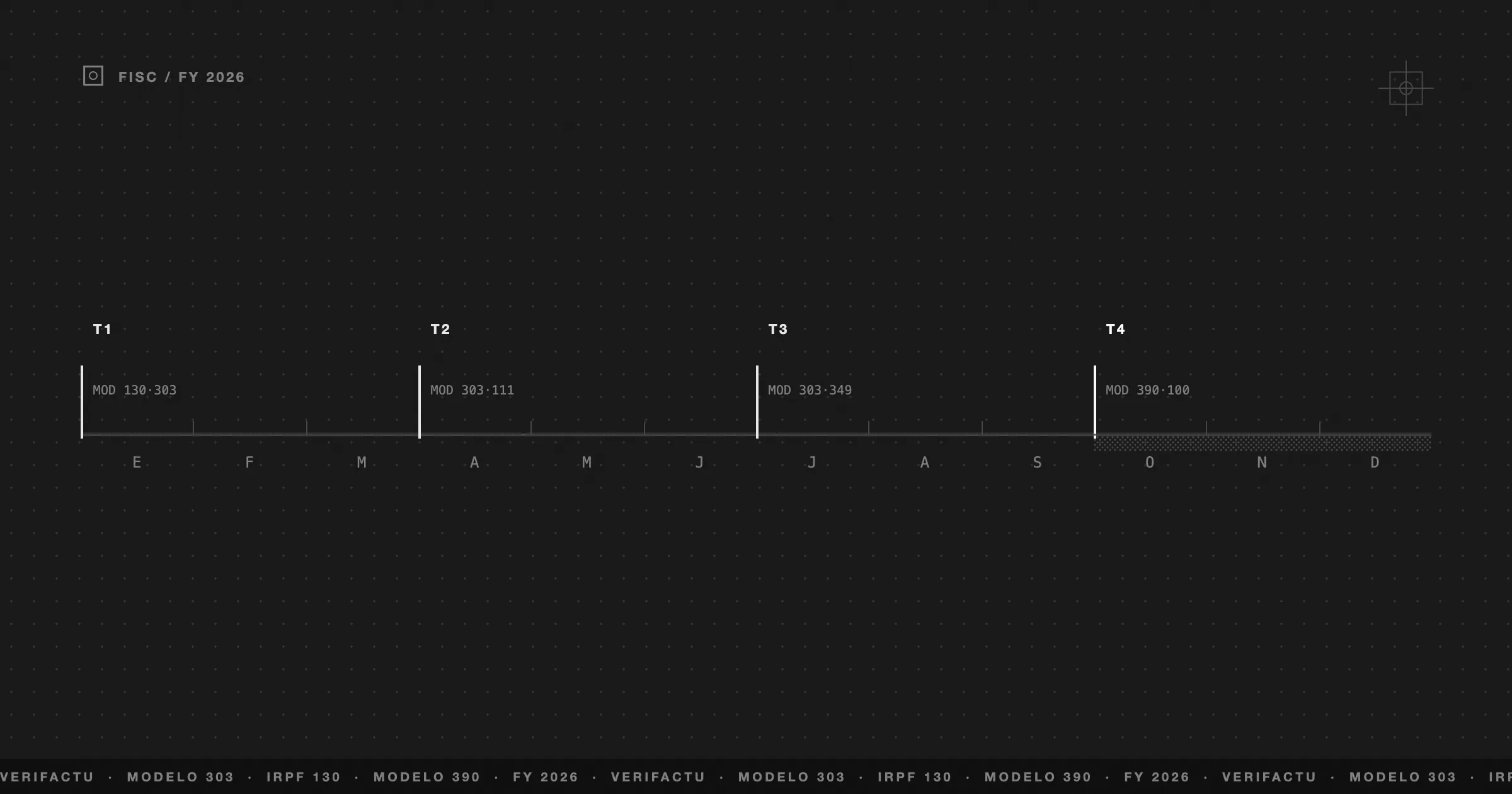

Exact Modelo 111 deadlines in 2026

In its quarterly form, Modelo 111 is filed within the first 20 calendar days of the month following each quarter:

| Quarter | Period | Filing window | With bank direct debit |

|---|---|---|---|

| Q1 | January - March | 1 to 20 April | Up to 15 April |

| Q2 | April - June | 1 to 20 July | Up to 15 July |

| Q3 | July - September | 1 to 20 October | Up to 15 October |

| Q4 | October - December | 1 to 20 January | Up to 15 January |

Q4 2025 was filed from 1 to 20 January 2026. Q4 2026 will be filed up to 20 January 2027.

In its monthly form, each return is filed within the first 20 days of the following month (the 15th with direct debit). When the last day of the window falls on a Saturday, Sunday or public holiday, the deadline moves to the next working day. Always check the AEAT taxpayer calendar for the specific month before treating a date as final.

The Modelo 111 boxes explained (01-30)

The form organises withholdings by type of income. Each block has three boxes: number of recipients, withholding base and amount withheld. It also distinguishes between income paid in cash (monetary) and income in kind.

| Income block | Cash | In kind |

|---|---|---|

| Employment income | 01-02-03 | 04-05-06 |

| Business and professional income | 07-08-09 | 10-11-12 |

| Prizes | 13-14-15 | 16-17-18 |

| Forestry proceeds | 19-20-21 | 22-23-24 |

| Assignment of image rights | 25-26-27 | — |

And the final settlement block:

| Box | What it captures |

|---|---|

| 28 | Sum of all withholdings and payments on account (total for the period) |

| 29 | To deduct: only in a supplementary self-assessment, the amount already paid previously |

| 30 | Amount payable (box 28 − box 29) |

In a normal return, box 29 is zero and box 30 matches box 28. Box 28 is the one that matters for the annual reconciliation with Modelo 190.

IRPF withholding rates in force in 2026

The applicable rates are those in the official AEAT table for 2026. There is no single percentage: it depends on the type of income.

| Type of income | 2026 withholding |

|---|---|

| Employment income | Progressive scale (based on pay and personal circumstances) |

| Company directors and board members | 35% (19% if the paying entity’s net turnover is below EUR 100,000) |

| Courses, lectures, seminars | 15% |

| Professional activities | 15% standard; 7% for the start-up year and the two following |

| Income obtained in Ceuta and Melilla | The withholding rate is reduced by 60% where the income qualifies for the art. 68.4 LIRPF deduction (art. 101 LIRPF) |

| Agricultural and livestock activities | 2% standard; 1% for pig fattening and poultry |

| Forestry activities (business activity, boxes 07-12) | 2% |

| Flat-rate (modulos) business activities | 1% |

| Forestry proceeds from public woodlands (capital gain, boxes 19-24) | 19% |

| Prizes | 19% |

The withholding on payroll is not a fixed percentage: it is calculated on a progressive scale that takes into account each worker’s expected annual pay and their personal and family circumstances.

Ceuta and Melilla are Spanish autonomous cities in North Africa with a special tax regime: income obtained there that qualifies for the art. 68.4 LIRPF deduction has its withholding rate reduced by 60% (art. 101 LIRPF). “Modulos” is Spain’s simplified, objective-estimate regime for small business activities.

How Modelo 111 relates to the annual summary, Modelo 190

Modelo 111 and Modelo 190 are two sides of the same obligation.

- Modelo 111 is the periodic payment self-assessment: each quarter (or month) you pay what you withheld.

- Modelo 190 is the informational annual summary: it involves no payment, but details, recipient by recipient, every withholding applied during the year.

The control point is the reconciliation: the sum of box 28 across your four Modelo 111 filings for the year must match the total declared in Modelo 190. If they do not match, the Tax Agency will spot it.

Common mistakes and how Frihet automates the calculation

These are the slip-ups that generate the most queries from the tax authority:

Putting rent into Modelo 111. Withholdings on the leasing of urban property go in Modelo 115, never in Modelo 111.

Modelo 111 vs Modelo 190 mismatch. If the annual sum of box 28 does not match Modelo 190, an incident is raised. It is the most expensive error to fix after the fact.

Applying the start-up professional rate incorrectly. The 7% only covers the year business activity starts and the two following; after that it returns to 15%.

Confusing the legal basis. Modelo 111 is governed by Order EHA/586/2011 and the IRPF Regulation. Do not rely on rules unrelated to the form to justify deadlines or boxes.

With Frihet, every payroll run and every expense invoice with a withholding that you record feeds the Modelo 111 calculation in real time:

All of it for organisations of any size: from the one filing a quarterly Modelo 111 with two payslips to the one declaring monthly for exceeding the large-company threshold. The figures are already calculated and ready to transfer to the AEAT electronic filing portal.

If you want to anticipate the impact of withholdings on your cash flow, the quarterly tax estimate and the tax calculator give you a quick snapshot. And to prepare for the shift to verifiable invoicing, review the guide to Verifactu in Spain.

To complete the map of your quarterly forms, you also have the guide to Modelo 303 for VAT and the guide to calculating your self-employed IRPF in 2026.

Was this article helpful?

FAQ

Who has to file Modelo 111?

Every individual, company and entity required to withhold or make payments on account under art. 76 of the IRPF Regulation: any organisation that pays employment income, income to professionals, prizes, forestry proceeds from public woodlands, or fees for the assignment of image rights. It is not exclusive to the self-employed.

Is Modelo 111 quarterly or monthly?

As a general rule it is quarterly. It is mandatory monthly for large companies (turnover above EUR 6,010,121.04 in the previous calendar year) and for public administrations with an annual budget above EUR 6 million.

What are the 2026 deadlines for Modelo 111?

In its quarterly form it is filed within the first 20 calendar days of the month following the quarter: up to 20 April, 20 July, 20 October and 20 January 2027. Q4 2025 was filed from 1 to 20 January 2026. If you pay by direct debit, the deadline moves forward to the 15th.

How does Modelo 111 relate to Modelo 190?

Modelo 111 is the periodic self-assessment through which you pay the withholdings applied; Modelo 190 is the informational annual summary, broken down per recipient. The sum of box 28 across the four Modelo 111 filings for the year must reconcile with the total in Modelo 190. The Modelo 190 for the 2025 tax year was filed from 1 January to 2 February 2026.

What withholding rates apply in Modelo 111 in 2026?

Employment income is withheld on a progressive scale, with special rates such as 15% for courses and lectures or 35% for company directors (19% if turnover is below EUR 100,000). Professionals withhold 15% as standard (7% for the start-up year and the two following). Other activities: agricultural and livestock 2% (1% for pig fattening and poultry), forestry 2%, flat-rate (modulos) 1% and prizes 19%.