Self-Employed IRPF Guide 2026: How to Calculate and Declare It Step by Step

Calculate your 2026 self-employed IRPF without errors. We explain retentions, Modelo 130, and how to declare it quarterly. Control your taxes.

TL;DR: Calculate your 2026 self-employed IRPF without errors. We explain retentions, Modelo 130, and how to declare it quarterly. Control your taxes. IRPF taxes your real profit (income minus expenses), not your gross turnover. Management is carried out throughout the year through retentions on invoices and/or quarterly payments (Modelo 130).

Key takeaways

- IRPF taxes your real profit (income minus expenses), not your gross turnover. Management is carried out throughout the year through retentions on invoices and/or quarterly payments (Modelo 130).

- An expense is deductible only if it is 100% linked to your activity, you have a complete invoice to justify it, and you have recorded it accounting-wise. Thorough expense control is the most effective way to legally reduce your IRPF payment.

- Automation with Frihet eliminates human error, saves dozens of hours per quarter, and transforms tax obligations into a financial planning tool. The data for your Modelo 130 is generated in real-time and with a single click.

Contents

Understanding IRPF for self-employed individuals: what it is and how it affects you

Managing self-employed IRPF is one of the most important and often most confusing tax responsibilities for self-employed professionals in Spain. Far from being an annual formality, IRPF is a constant obligation managed throughout the year that directly impacts your liquidity and financial planning. Understanding how it works is not just a legal obligation, but a strategic tool to optimize your tax burden and ensure the health of your business.

IRPF, or Impuesto sobre la Renta de las Personas Físicas (Personal Income Tax), is a personal, progressive, and direct tax that levies the income you have earned during a calendar year. As a self-employed individual, this “income” refers to your profits, not your total turnover. This is the first key concept you must master: Hacienda (the Spanish Tax Agency) does not charge you for what you earn, but for your net income, which is the difference between your computable income and your deductible expenses. Therefore, thorough control of your expenses is fundamental.

To ensure that the State collects this tax in advance and to prevent you from having to make a massive payment in the annual Income Tax declaration, there are two main advance payment systems: retentions on invoices and quarterly fractional payments through Modelo 130. Depending on the nature of your clients and your professional activity, you will be subject to one, the other, or a combination of both. Understanding your situation is the first step to correctly fulfilling your obligations.

An incorrect calculation or late submission of your IRPF obligations can lead to penalties, surcharges, and late payment interest from the Tax Agency. These errors not only entail an economic cost but also a source of stress and lost time. The key to avoiding them is organization and the use of appropriate tools that allow you to have a clear and real-time view of your tax situation. To get off to a good start, it is essential to know how to control your freelancer expenses, as every deductible euro counts.

Self-employed IRPF retention: when and how to apply it

IRPF retention is one of the most common advance payment mechanisms for self-employed professionals. It works as an advance payment that your client makes on your behalf. When you issue an invoice to another company or self-employed individual established in Spain, you include a retention percentage that is subtracted from the total amount to be collected. Your client does not pay this amount to you; instead, they have the legal obligation to deposit it with the Tax Agency on your behalf.

For the year 2026, the general retention rate for most professional activities is 15%. This means that if you issue an invoice with a taxable base of €1,000, you will apply a retention of €150, and the net amount you will receive will be €850 (plus the corresponding IVA). This system simplifies your management, as your client is responsible for making that payment to Hacienda for you.

There is an important advantage for new professionals. If you start your activity, you can benefit from a reduced retention rate of 7%. This measure can be applied during the year you register and in the two subsequent calendar years, provided you have not carried out any professional activity in the previous twelve months. Applying this 7% can give you much-needed liquidity in the early stages of your business, although you should bear in mind that it will imply a higher payment in your annual Income Tax declaration, as you have advanced fewer taxes.

It is crucial to know when you should NOT apply retention. The main rule is that it only applies to invoices issued to other professionals or companies within Spanish territory. Therefore, the following are excluded:

- Invoices to private clients: Individuals who do not act as entrepreneurs or professionals are not obliged to apply retentions.

- Invoices to foreign clients: Companies or individuals located outside of Spain are not subject to the Spanish retention system.

- Self-employed individuals under objective estimation (módulos): Certain business activities, not professional ones, are taxed under a different system and do not apply retentions on their sales invoices (although they do bear them on certain purchases).

Incorrectly applying a retention, or not doing so when it is mandatory, is one of the 5 invoicing errors that cost the most money. Make sure that your invoicing software, such as Frihet, allows you to configure the correct retention type for each client, thus avoiding problems for both you and your clients, who are ultimately responsible for paying it.

The quarterly fractional payment: Modelo 130

If your profile as a self-employed individual does not fit into the retention system, or if retentions represent a minority of your income, Modelo 130 comes into play. This is the form you will use to make your fractional IRPF payments directly to the Tax Agency each quarter. The general rule is clear: if more than 70% of your professional income from the previous year was not subject to retention, you are obliged to submit Modelo 130.

This is very common for self-employed individuals whose clients are mainly private individuals (a psychologist, a plumber, a private tutor) or foreign companies (a software developer working for a startup in the USA). In these cases, since no one withholds IRPF from you, you are the one who must calculate and pay the corresponding advance payments on your profits.

The calculation of Modelo 130 is based on your accumulated net income from the beginning of the year until the end of the quarter you are declaring. On this figure, you must pay 20%. For example, for the second-quarter declaration, you will sum all your income and subtract all your expenses from January 1st to June 30th. You will then apply 20% to the result. From this amount, you can subtract payments you made in previous quarters and any retentions that other clients may have applied to you (if applicable).

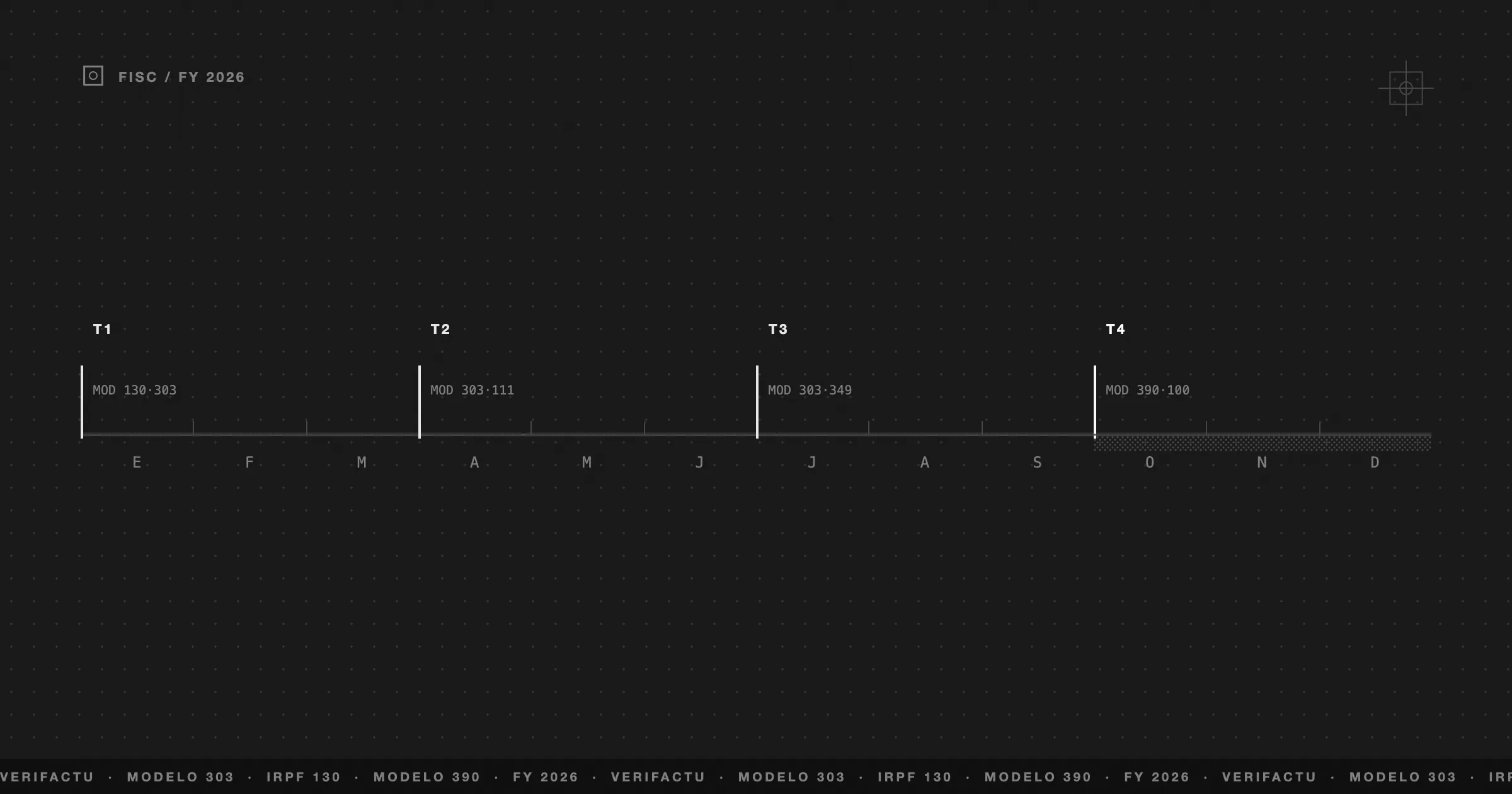

TAX CALENDAR

The deadlines for submitting and paying Modelo 130 are non-extendable. Mark them on your calendar to avoid surcharges:

- First quarter (1Q): from April 1st to 20th.

- Second quarter (2Q): from July 1st to 20th.

- Third quarter (3Q): from October 1st to 20th.

- Fourth quarter (4Q): from January 1st to 30th of the following year.

Not submitting Modelo 130 when obliged is a serious tax infringement. Therefore, it is vital that at the beginning of each fiscal year, you analyze your invoicing from the previous year and determine if you exceed that 30% threshold of income with retention. If not, the quarterly submission of Modelo 130 becomes your primary IRPF obligation.

How to calculate your net income step by step

The core of any self-employed IRPF calculation, whether for Modelo 130 or for your annual declaration, is net income. This figure represents your real profit and is the basis on which taxes are applied. The formula is simple in theory but requires meticulous record-keeping in practice: Net Income = Computable Income - Deductible Expenses.

Computable income is the sum of the taxable bases of all invoices you have issued during the corresponding period (the quarter for Modelo 130). It is important to note that it is governed by the accrual principle, not the cash basis. This means you must include income from invoices issued in that quarter, even if you have not yet collected them. It includes all sales of goods and provision of services that constitute the object of your activity.

On the other hand, deductible expenses are the key to optimizing your tax burden. These are all costs that are directly and unequivocally related to the development of your economic activity. The Tax Agency requires them to meet three fundamental requirements: they must be linked to the activity, they must be justified with a complete invoice, and they must be accounting-wise recorded in your expense books.

The list of deductible expenses is extensive, but some of the most common include:

- Social Security contributions: The self-employed quota is 100% deductible.

- Rent: The rent for your office, commercial premises, or coworking space.

- Utilities: Electricity, water, internet, telephone. If you work from home, you can deduct 30% of the proportional part of the home you use for your activity.

- Services from independent professionals: The fees of your accountant, lawyer, marketing consultant, etc.

- Software and subscriptions: Tools like Frihet, software licenses, subscriptions to platforms necessary for your work.

- Advertising and marketing: Expenses on Google Ads campaigns, social media, flyer design, etc.

- Insurance: Civil liability insurance, health insurance (with an annual limit).

- Amortizations: The depreciation of assets such as computers, machinery, or vehicles used for the activity.

To illustrate the importance of good expense record-keeping, let’s look at a comparative table of common expenses and their particularities when it comes to deducting them.

| Type of Expense | Main Requirement | Example of Justification | Level of Deductibility |

|---|---|---|---|

| Self-employed quota | Being registered with RETA. | Bank receipt of payment. | 100% deductible |

| Office rent | Rental contract in the name of the self-employed individual or company. | Monthly invoice from the landlord. | 100% deductible |

| Utilities (office) | Invoices in the name of the activity holder. | Electricity, water, internet bills. | 100% deductible |

| Utilities (home) | Having the home partially dedicated to the activity. | Direct-debited bills. | 30% on the proportion of m² dedicated |

| Software (e.g., Frihet) | Exclusive use for professional activity. | Subscription invoice. | 100% deductible |

| Business meals | Card payment, on a working day, and with clients/suppliers. | Simplified invoice (ticket) and proof of payment. | Deductible with daily limits |

| Vehicle and fuel | Exclusive dedication to the activity (difficult to prove). | Purchase invoices, repairs, fuel. | Generally 50% of IVA, IRPF very restrictive (except for commercial agents, transporters, etc.) |

Simplify your IRPF calculation

Frihet automatically categorizes your expenses and gives you your net income in real time. Stop struggling with spreadsheets and take control of your taxes.

Submitting Modelo 130: from calculation to declaration

Once you have calculated your accumulated net income for the quarter, the next step is to transfer that information to the Tax Agency. The process of submitting Modelo 130 is entirely telematic and requires you to securely identify yourself on the AEAT Electronic Headquarters.

To access, you will need one of the accepted identification systems: the digital certificate, the electronic DNI, or the Cl@ve PIN system. Once inside the portal, look for the Modelo 130 procedure and select the submission option for the corresponding fiscal year and period. A web form will open that you must fill in with the data you have already calculated.

The key fields you will need to complete are:

- Box [01]: Here you will enter the total computable income accumulated from the beginning of the year until the end of the quarter.

- Box [02]: In this box, you will enter the total deductible expenses accumulated during the same period.

- Box [03]: The form will automatically calculate the net income (Box 01 - Box 02).

- Box [04]: Here, 20% is applied to the net income to obtain the initial quota.

- Boxes [05] and [06]: Used to subtract payments from previous quarters and retentions borne during the year.

- Box [07]: This is the final result of the calculation, the amount to be paid in this quarter.

After filling in all the fields and verifying that the data is correct, the system will show you the final result. This can be one of three types: to be paid, if you have to pay Hacienda; negative or to be deducted, if your expenses exceed your income (the result will be offset in future quarters); or zero, if the result is null. If the result is to be paid, you will have to proceed with the payment.

For payment, you have two main options. The most convenient is direct debit, which you can select if you submit the model within the first 15 days of the declaration period (for example, until April 15th for Q1). If you submit later or prefer another option, you can generate an NRC (Complete Reference Number), which is a code you obtain after making the payment directly through the AEAT payment gateway or your collaborating bank’s online banking. Once you have the NRC, you enter it into the form and finalize the submission.

Stop calculating by hand: how Frihet automates your taxes

Manual calculation of self-employed IRPF using spreadsheets is a widespread practice, but inherently risky and terribly inefficient. A simple formula error, a forgotten invoice, or a wrongly categorized expense can completely distort your calculation, leading you to overpay or, worse still, receive a penalty from Hacienda. The time you spend collecting receipts, reviewing bank movements, and adding figures is time you don’t dedicate to growing your business.

Migrating from a manual system to an integrated management platform is a qualitative leap in professionalizing your activity. As we detail in our guide on how to move from Excel to an ERP, centralizing your financial information not only drastically reduces the risk of human error but also provides you with visibility that a spreadsheet can never offer.

This is where a platform like Frihet completely transforms your relationship with taxes. Frihet securely connects to your bank accounts and automatically reconciles each income with its corresponding sales invoice. At the same time, it captures and categorizes your expenses, learning from your patterns so that management becomes increasingly autonomous. The result? Your net income is calculated in real time, every day of the year.

When it’s time to submit Modelo 130, you don’t have to start a three-month financial archaeology process. You simply access your real-time financial dashboard in Frihet, select the period, and the platform provides you with the exact figures you need for boxes [01] and [02]. What once took hours of stress and double-checking is now resolved in less than five minutes with full confidence in the data’s accuracy.

This automation goes beyond simply filing taxes. It allows you to have constant tax foresight, knowing at all times how much IRPF you are generating. This helps you plan your cash flow, avoid unpleasant surprises, and make smarter business decisions based on up-to-date and reliable data. Moving from being reactive to proactive in tax management is the competitive advantage that technology offers you.

Take definitive control of your IRPF

Discover how thousands of self-employed individuals have left spreadsheets behind and manage their taxes in minutes with Frihet. Your time is too valuable to spend on bureaucracy.

Frequently Asked Questions

What happens if my retentions are greater than the Modelo 130 payment?

In the calculation of Modelo 130, the retentions applied to you are subtracted from the fractional payment. If the amount of withheld retentions is greater than 20% of your net income, the result of the model will be zero or negative, so you will not have to pay anything in that quarter.

Do all self-employed individuals have to submit Modelo 130?

No. You are only obliged to submit Modelo 130 if, in the previous year, more than 70% of your income was not subject to retention. If the majority of your invoices (more than 70%) are addressed to Spanish companies and include the corresponding retention, you do not have to submit this quarterly model.

What expenses can I deduct for IRPF as a self-employed individual?

You can deduct any expense that is directly related to your economic activity, is duly justified with a complete invoice, and is accounting-wise recorded. This includes the self-employed quota, office rent, utilities, software, marketing, professional services, insurance, and many others.

How does quarterly IRPF affect my annual Income Tax declaration?

All payments you make through Modelo 130 and all retentions applied to you during the year are advance payments towards your annual IRPF. When making your Income Tax declaration (Modelo 100), your final IRPF amount for the entire year will be calculated, and all these advance payments will be subtracted. The final result will be either payable, if you advanced less than due, or refundable, if you advanced more than due.

Was this article helpful?

FAQ

What happens if my retentions are greater than the Modelo 130 payment?

In the calculation of Modelo 130, the retentions applied to you are subtracted from the fractional payment. If the amount of withheld retentions is greater than 20% of your net income, the result of the model will be zero or negative, so you will not have to pay anything in that quarter.

Do all self-employed individuals have to submit Modelo 130?

No. You are only obliged to submit Modelo 130 if, in the previous year, more than 70% of your income was not subject to retention. If the majority of your invoices (more than 70%) are addressed to Spanish companies and include the corresponding retention, you do not have to submit this quarterly model.

What expenses can I deduct for IRPF as a self-employed individual?

You can deduct any expense that is directly related to your economic activity, is duly justified with a complete invoice, and is accounting-wise recorded. This includes the self-employed quota, office rent, utilities, software, marketing, professional services, insurance, and many others.

How does quarterly IRPF affect my annual Income Tax declaration?

All payments you make through Modelo 130 and all retentions applied to you during the year are advance payments towards your annual IRPF. When making your Income Tax declaration (Modelo 100), your final IRPF amount for the entire year will be calculated, and all these advance payments will be subtracted. The final result will be either payable, if you advanced less than due, or refundable, if you advanced more than due.